Term life insurance is a pivotal component of financial planning for many individuals and families. This type of insurance provides coverage for a specified term and can offer substantial benefits for those seeking cost-effective protection. This comprehensive guide will walk you through everything you need to know about term life insurance, including its features, benefits, top providers, and practical buying tips.

What is Term Life Insurance?

Term life insurance is designed to provide financial protection for a predetermined period. Unlike permanent life insurance, which lasts for the policyholder’s entire life, term life insurance is set for a specific number of years, such as 10, 20, or 30 years.

Features of Term Life Insurance

Fixed Premiums

One of the key features of term life insurance is its fixed premiums. This means that the amount you pay for coverage remains the same throughout the term of the policy. This stability allows you to budget more effectively and avoid unexpected increases in your insurance costs.

Flexibility in Terms

Term life insurance offers flexibility in choosing the length of coverage. You can select a term that aligns with your specific needs, whether it’s covering the years until your mortgage is paid off or until your children are financially independent.

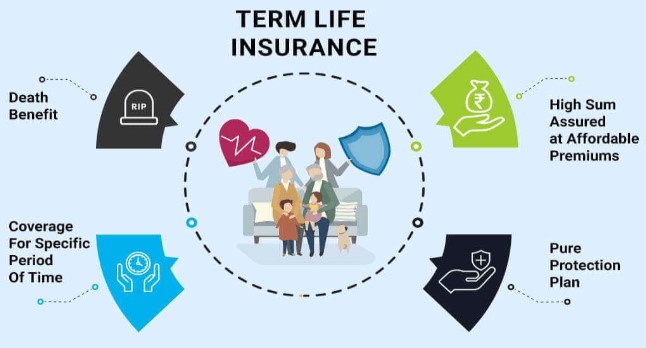

Death Benefit

The primary feature of term life insurance is the death benefit. If the policyholder passes away during the term of the policy, their beneficiaries receive a lump sum payment. This payout can be used to cover living expenses, debt repayment, and other financial needs.

Renewability and Convertibility

Many term life insurance policies offer the option to renew or convert the policy after the term ends. Renewal allows you to extend coverage, often at a higher premium, while convertibility provides the opportunity to switch to a permanent life insurance policy without additional medical underwriting.

Benefits of Term Life Insurance

Term life insurance is valued for several key benefits, making it an attractive option for many individuals and families.

Affordable Premiums

One of the most significant advantages of term life insurance is its affordability. Compared to permanent life insurance, term policies generally have lower premiums. This cost-effectiveness makes it possible to obtain substantial coverage without straining your budget.

Simplicity and Transparency

Term life insurance is straightforward and easy to understand. Unlike permanent life insurance, which often includes complex investment components and cash value accumulation, term life insurance focuses solely on providing a death benefit. This simplicity means fewer surprises and easier management.

Flexibility in Coverage

The flexibility of term life insurance is another major benefit. With various term lengths available, you can choose a policy that aligns with your specific financial goals and obligations. Whether you need coverage for a short period or several decades, term life insurance can be tailored to your needs.

Ability to Customize Policies

Many term life insurance providers offer customizable policies, allowing you to add riders and adjust coverage options to better suit your needs. This customization can enhance your policy and provide additional benefits, such as accelerated death benefits or waiver of premium riders.

Financial Protection for Dependents

Term life insurance provides essential financial protection for dependents. In the event of the policyholder’s death, the death benefit can be used to support surviving family members, covering expenses such as living costs, education, and debt repayment.

Types of Term Life Insurance Policies

Term life insurance policies come in various forms, each with unique features and benefits. Understanding these types can help you select the most suitable policy for your needs.

Level Term Life Insurance

Level term life insurance is the most common type of term policy. With this option, the premium and death benefit remain constant throughout the term of the policy. This predictability makes budgeting easier and ensures consistent coverage.

Decreasing Term Life Insurance

Decreasing term life insurance is designed to provide a death benefit that decreases over time. This type of policy is often used to cover a mortgage or other debt that decreases over time. As the debt reduces, so does the death benefit, reflecting the reduced financial risk.

Increasing Term Life Insurance

Increasing term life insurance offers a death benefit that increases over time. This type of policy is useful for individuals who expect their financial responsibilities to grow, such as increasing living expenses or future educational costs. The increasing benefit helps keep pace with inflation and rising costs.

Convertible Term Life Insurance

Convertible term life insurance provides the option to convert your term policy to a permanent life insurance policy without undergoing additional medical underwriting. This flexibility can be valuable if you decide to extend your coverage beyond the initial term.

Renewable Term Life Insurance

Renewable term life insurance allows you to renew your policy at the end of the term, often without needing to provide additional medical information. This option can be beneficial if you want to maintain coverage beyond the initial term but are concerned about potential health changes.

Top Providers of Term Life Insurance

Selecting the right provider is crucial for obtaining a term life insurance policy that meets your needs. Here are some of the top providers, known for their reliable coverage and competitive rates.

State Farm

State Farm is a well-known provider with a strong reputation for customer service and financial stability. They offer a variety of term life insurance options with customizable terms and affordable rates.

Pros

- Flexible term options

- High customer satisfaction

- Strong financial stability

Cons

- Potentially higher premiums for certain age groups

Price

Starting at approximately $10 per month, depending on the policy and coverage amount.

Features

- Renewable policies

- Conversion options

- Online quotes and easy application process

Geico

Geico is recognized for its competitive rates and user-friendly online management. Their term life insurance policies are designed to be accessible and affordable.

Pros

- Competitive rates

- Easy online application process

Cons

- Limited customization options compared to some competitors

Price

Starting at around $15 per month, depending on coverage and term length.

Features

- Instant quotes

- Online account management

Prudential

Prudential offers extensive coverage options with a strong financial reputation. Their term life insurance policies come with various riders and customization options.

Pros

- Extensive coverage options

- Strong financial reputation

Cons

- Higher premiums for older applicants

Price

Starting at approximately $20 per month, depending on the policy and coverage.

Features

- Customizable policies

- Additional riders for enhanced coverage

TermLife2Go

TermLife2Go specializes in affordable and straightforward term life insurance policies. They offer a range of options with an emphasis on simplicity and ease of application.

Pros

- Affordable rates

- Easy application process

Cons

- Limited customer service compared to larger providers

Price

Starting at around $12 per month, depending on coverage and term length.

Features

- Quick quotes

- Flexible term lengths

Haven Life

Haven Life, backed by MassMutual, provides modern, digital-friendly term life insurance policies. They focus on convenience and competitive pricing.

Pros

- User-friendly online application

- Competitive rates

Cons

- Limited in-person customer service

Price

Starting at approximately $18 per month, depending on the policy and coverage.

Features

- Digital application

- Instant coverage decisions

Comparison Table

| Provider | Use Case | Pros | Cons | Price | Features |

|---|---|---|---|---|---|

| State Farm | Comprehensive coverage | Flexible terms, high customer satisfaction | Higher premiums for older ages | From $10/month | Renewable policies, conversion options |

| Geico | Budget-friendly options | Competitive rates, easy online management | Limited customization options | From $15/month | Instant quotes, online management |

| Prudential | Extensive coverage options | Strong financial reputation, customizable | Higher premiums for older applicants | From $20/month | Customizable policies, additional riders |

| TermLife2Go | Affordable and easy application | Wide range of options, easy application | Limited customer service | From $12/month | Quick quotes, flexible terms |

| Haven Life | Modern, digital-friendly policies | Easy online application, competitive rates | Limited in-person service | From $18/month | Digital application, instant coverage |

How to Buy Term Life Insurance

Purchasing term life insurance involves several steps. Here’s a comprehensive guide to help you through the process.

Step 1: Research Providers

Begin by researching different insurance providers to find those that offer term life insurance policies. Look for providers with strong financial ratings and positive customer reviews. Consider factors such as coverage options, premiums, and policy features.

Step 2: Get Quotes

Use online tools and insurance comparison websites to obtain quotes from various providers. Compare the quotes based on coverage amount, term length, and premiums. This will help you identify the best options for your needs and budget.

Step 3: Evaluate Policy Options

Review the policy options available from your chosen providers. Consider factors such as term length, coverage amount, and any additional riders or features. Ensure that the policy aligns with your financial goals and provides the necessary protection.

Step 4: Apply for Coverage

Once you have selected a policy, complete the application process. This may involve providing personal information, undergoing a medical exam, and answering health-related questions. The application process varies by provider, so follow their specific instructions.

Step 5: Review and Finalize

Carefully review the terms and conditions of your policy before finalizing the purchase. Ensure that all details are accurate and that you understand the coverage and any exclusions. Once satisfied, finalize your policy and begin making premium payments.

FAQs About Term Life Insurance

1. What is the difference between term life insurance and whole life insurance?

Term life insurance provides coverage for a specific period, while whole life insurance offers coverage for the policyholder’s entire life. Whole life insurance also includes a cash value component that grows over time, unlike term life insurance.

2. Can I convert my term life insurance policy to a permanent policy?

Many term life insurance policies offer a conversion option, allowing you to switch to a permanent policy without additional medical underwriting. Check with your provider to see if this option is available with your policy.

3. How long should I buy term life insurance for?

The length of your term policy should align with your financial responsibilities and goals. Common term lengths are 10, 20, or 30 years, but you can choose a term that fits your specific needs.

4. Are term life insurance premiums tax-deductible?

No, term life insurance premiums are generally not tax-deductible. However, the death benefit paid to beneficiaries is typically tax-free.

5. What happens if I outlive my term life insurance policy?

If you outlive your term life insurance policy, the coverage will expire, and no death benefit will be paid. Some policies offer renewal or conversion options to extend your coverage.

Conclusion

Term life insurance is a valuable tool for providing financial protection for a specific period. With its affordability, simplicity, and flexibility, it can be an excellent choice for individuals and families seeking cost-effective coverage. By understanding the features, benefits, and options available, you can make informed decisions and select the policy that best meets your needs.

Whether you’re looking for a basic policy or one with customizable features, this guide has equipped you with the knowledge to navigate the world of term life insurance. Use the insights provided to find the right policy and ensure that your loved ones are protected.